25,000

New Leads

The number of subscribers that came directly from the campaign

$0

Ads Budget

Amount spent per day on paid ads

33%

Conversion Rate

Percentage of traffic that converted on the landing page

60%

Leads from sharing

Leads that came directly from other leads sharing the campaign

Key Takeaways

Show up and have something to offer!

Show Up

Mush showed up for a job he wasn't qualified for on paper because he knew he had something to offer.

Find the Right Conditions

Being in Puerto Rico allowed Zenus to leverage regulations friendly to the international banking business they wanted to build.

Find your Demographics

Talk to your waitlist and find out who are going to be your best customers.

Keep Rewards Simple and Offer Free Product

Zenus rewards people for sharing their campaign with months of free service. Simple and effective.

Understand The Value of a Lead

In a space where it can cost up to $2,000 to acquire a financial customer you can afford to reward people a lot for referrals.

Believe in Yourself

Have confidence. You can learn what you need on the fly. You need to believe in yourself first before somebody else recognizes your skills.

"We built a nice website and used the waitlist campaign methods that for example, Robinhood had practiced, and the Dollar Shave Club's done."

"We have around 25,000 people on our waiting list. And again, this has been fruits of organic growth. Like you said, 58 almost 60% of leads come from existing waitlist customers sharing their link."

Campaign Goal:

Increase interrest using prelaunch waitlist campaign.

Key Features Used:

- KickoffLabs Actions

- Friend Referral Tracking

- Reward Levels

- Emails

- Viral Boost

"Our (waitlisted) clients have given us a lot of new ideas on what we need to focus. Essentially, we're using this tool to figure out what is the low hanging fruit, what is our perfect demographic?"

Contest Type(s): waitlist - reward levels

Interview Bio

Mushegh Tovmasyan - Founder - Zenus

FinTech entrepreneur and a veteran of the online trading industry with international C-Level management experience. A serial entrepreneur at heart, Mushegh has a good eye for spotting individual talent and untapped opportunities in the market. He has been involved in a number of traditional M&A transactions on both sides of the table. He led acquisitions of various regulated financial services entities in North America, Europe, Asia and East Africa, and also raised funds for various projects in Finance, Technology, and the Sport & Hospitality space. He is the principal behind seed & venture capital firm Forexify most recently exiting from two successful ventures – Divisa Capital and Equiti Group in order to focus full time on Zenus Bank.

Full Transcript

Josh: Hi, I'm Josh Ledgard, and welcome to the On Growth Podcast from KickoffLabs. My goal with this podcast is to help you grow sustainable businesses through the stories of our customers and our team. This week we're sharing an interview with Mush Tovmasyan. Mush is the founder of Zenus, and they're in the middle of their launch campaign on KickoffLabs. So far with zero dollars spent on ads, the KickoffLabs campaign has collected over 25,000 email addresses at a 33% conversion rate, with a 60% viral boost. That means people are excited about Zenus, and they're telling their friends about it, using the KickoffLabs' referral links.

You're going to love this story about how he got his first job by showing up to interview for a position he was entirely unqualified for.

Josh: In this interview we'll dig into exactly how they've incentivized that sort of sharing. We'll also cover the hidden benefits of building a large waitlist early on while you're working on your product. Finally, you're going to love this story about how he got his first job by showing up to interview for a position he was entirely unqualified for and telling them exactly how he could help.

Josh: Be sure to check out the notes for this episode on our site because we've included a ton of images, used email copy and everything you need to recreate their success. Remember, if you enjoy this episode, subscribe to the KickoffLabs On Growth Podcast in Apple or your favorite podcast client. Write us a review and send any feedback to Josh@KickoffLabs.com. Also, if you want to go big with your idea, don't forget to sign up at KickoffLabs.com to start building your audience today. Onto the show.

Josh: All right, we are live and I am here with Mush and his product is Zenus. And Mush, before we get into the product, tell me a little bit about your background and how you got to this point where you're working on this product launch.

Mush: Yeah, a pleasure, Josh. Well, I guess a bit about me, I was at the right time at the right place at the beginning of the decade of 2000 when online trading went digital. So I guess it was the beginning of this fintech era that has touched on everybody's life. And that journey, I started in the online trading space, brokerage, currency trading, derivatives, futures. And I saw and led a lot of the key developments that have made life easier for millennials and pretty much everyone, society, that's propagated around the world.

Mush: I started my career in California, San Diego, and then San Francisco and Orange County. But then with changes of regulation ...

Josh: What did you start doing? What was your role when you started working?

Mush: It's actually pretty funny. I showed up at this brokerage house while I was still in school, and I showed up to this job interview for a research analyst, I believe. And they were like, "Do you have a degree?" And I said, "No." They said, "Do you have experience in this?" I said, "No." "Can you work full-time?" I said, "No, I'm in school." And the CEO was, "What are you doing here? This is essentially, this job is not for you. Thank you. Goodbye." So I went home and I had done my research, I wrote a nice thank you email to the CEO saying, whatever, thank you for the opportunity looking forward, blah blah blah.

But then I added my two cents... your website isn't really user friendly. It seems like a little kid made it. So I immediately get a reply back saying, "Hey, can you come back tomorrow?

Mush: But then I added my two cents. I said, from what I understand, you're an online brokerage and your clients are all over the world and don't get me wrong, but your website isn't really user friendly. It seems like a little kid made it. So I immediately get a reply back saying, "Hey, can you come back tomorrow? And we want to talk further to you." And, I guess that was the beginning because then the questions are, can you figure this out if we show you this competitor in a different part of the world, can you figure out how they're doing that? We have a challenge, can you solve it?

Mush: And what dawned onto me is, was that these were 20, 30-year experienced professionals, that had seen from the stock floor traders in the way the exchanges were in the old days, all the way to moving big amounts of money internationally and whatnot, in their respective careers. But technology was so new to them and it was so difficult for them to understand. It was the opposite, I was a student studying finance and business and economics at school in San Francisco and I was born with technology and around technology. So even though I didn't know exactly, how they're used to do things, I knew what where they wanted to get to. And I knew what's available with modern technology and resources. So it was pretty easy for me to put the two together.

Within pretty much six months I went from being this intern that didn't qualify for the lowest level job, to the guy that the whole company depended on.

Mush: And within pretty much six months I went from being this intern that didn't qualify for the lowest level job, to the guy that the whole company depended on. From there on, I moved on to other shops until I eventually created my own group of broker-dealers in the US. We expanded to Europe, we got regulated in seven countries. We serviced institutions, hedge funds all the way down to individual traders from over a hundred countries. And by the end of 2017 I essentially, I went into a joint venture with some previous colleagues from the industry and had an exit into a consortium of investors from the Middle East, a Saudi family office that bought my group of companies. Allowing me to move on and start on this new venture.

Josh: So I love that story, early on. So you showed up for a job that, I mean on paper you were not qualified for. And so what was it about you that made you show up? I mean, you knew that you had a sense of like, you knew innately that you could help them, right?

Mush: Yeah. I mean for me, I've always been an entrepreneur, since early on, since I guess when I was 10, 12. I was already doing websites and doing the early days of affiliate, and e-commerce and then digital marketing. So combining that with my education, I actually felt that what they're teaching me is already outdated. It was a very particular couple of years when the school system was teaching you something where in practice, it's already outdated. And it was very evident that it was outdated.

Mush: I guess I'm an ambitious person inside of me and the problem solver inside of me, I ended up at this brokerage and they saw the spark. And gave me the opportunity, which we both benefited, both sides.

Josh: Got it. You showed up, which people are scared to do in the first place in that situation, they wouldn't put themselves out there for a position they didn't think they were super qualified for. And then you were honest in terms of giving them feedback about things. I think that so few people are honest in those situations about how you could help and the situation that they're in. So they probably respected that a lot, I get the sense from their story.

Josh: So now you've led us up to Zenus. So tell us about the idea. So tell us about the product, what it is and what your goals are.

Mush: Yeah, so in the second half of that story where we are an online brokerage servicing oldest clients that were using their phones, tablets, their computers to trade billions and billions in dollars every day in foreign exchange. This is the world's biggest market. It's 24 hours. It does about, I don't know, five, six trillion a day in transactional volume. So we were a key provider in that space.

Mush: I realized that the world is extremely fragmented when it comes to access to financial services. $1,000 in the hands of an American in New York, buys him a lot more than the same thousand dollars in US dollar terms, in the hands of somebody in a third-world country. It would take a long conversation to get to the root cause of it. But the reality today, even today, is that there's a lot of fragmentation.

Mush: There's a lot of inequality in access to financial services, right? This is labeled as cross-border trading, payment services, cross-border transactions. And this issue or this need or this challenge is further propagated within today's society, right? Digital marketing is everywhere. Social networks are everywhere. Let's say in India, can be doing marketing for an online e-commerce shop that runs on Shopify, that's marketed to people sitting in Europe. And then they use PayPal to get paid. And then somehow they need to access the money that's in PayPal to spend it in their own country, to pay employees and whatnot. So we've become a very connected world.

Mush: But this challenge still exists because in my opinion, the core of this problem is the entity that's a bank. What we know of what a bank is, it's a very old concept of a local lender, right? The original need for a bank was to take money from one person and lend it to your neighbor. In today's society, there's been a lot more things put on banks, obligations, trading, and I don't know, all kinds of loans, cross-border issues and whatnot. And a lot of banks have challenged, have struggled to get there.

Mush: Part of it is digital transformation, which is a key trending keyword, I guess, it's a buzzword in the last few years. Because every bank in every country is going through this digital transformation, which is to reinvent themselves and modernize their technology for today's society. But at the same time, banks have a lot of incumbent tech, their old business models. It's pieced together over decades and decades. So it's very hard for that institution to reinvent itself.

Mush: But banking is also one of the most regulated businesses you can get into. The barrier of entry to actually get a regulator to approve the shareholders of the bank, the management of the bank, the business model of the bank, the amount of money required to get to all of this, and the amount of time that it takes to get this set up, it's very difficult. And this has created a new wave, which is called challenger banking in a lot of parts of the world. Europe and UK are leaders, that have managed to I guess expand the regulation to allow newer business models.

Mush: And essentially what a challenger bank is looking to do is, it's a very modern front-end, but it's based on a traditional bank. It's a piggybacked business model. So, where they are able to solve the front-end of the problem, having a much more appealing interface, whether it's for millennials or today's society, have all the cool features be adapted to every type of mobile device there is. Whether it's the watch or the phone and things like that. It's only the first leg of the journey. They still have to depend on the deposit taker, which is the traditional banking institution, which in my opinion is the source of this problem, right? This limitation of transacting cross-border.

I found my solution in Puerto Rico.I found regulation that allows me to, from one bank essentially service US clients in any US state, but at the same time international clients from any non-sanctioned country.

Mush: So what I wanted to do is essentially to find a solution to this problem. And I researched every major regulation there exists from UK to Europe to all the money centers, Australia, Singapore, Hong Kong, whatever, US, and all the offshore jurisdictions. And essentially found my solution in Puerto Rico, which is very interesting because Puerto Rico, a lot of people aren't very aware of the structure. It's a US territory. It's not an independent country. Puerto Ricans are US passport holders. And Puerto Rico does not have a central bank. It does not have its own currency or its borders. Right? It's just like a state of the US from that perspective.

Mush: But being a territory, it has its own unique flavor. It has to follow federal regulations, but it has a local governmental entity tasked with enforcing US federal rules. So in here I found regulation that allows me to, from one bank essentially service US clients in any US state, but at the same time international clients from any non-sanctioned country. And essentially for me, this is not new because a broker, that's what brokers are able to do.

Mush: E-Trade is able to take from one entity, their US E-Trade accounts. They can own customers from China or from Australia or from the US. Same goes for Robinhood. But banks traditionally have never been able to do this. In Europe for example, you need to have a residency permit or a job offer to be able to open a bank account in a European bank. So if you're a foreigner traveling there on holiday, no bank will give you an account. In the US it's a bit more easier because if you show up physically into let's say a Wells Fargo or at JP Morgan branch in the US, and bring your foreign identification and foreign proof of address and whatnot, most likely you will be able to open an account.

Mush: But my solution is essentially something that's never been done in the world. We're calling ourselves the first US bank that allows any foreigner to open an account, a US bank account remotely. So imagine, somebody sitting in Argentina or in China or in India or in Europe can download our app or go through our website, and within a few minutes provide us all the required information needed for us to meet US regulatory requirements. And for us to be able to remotely confirm their identity, make sure that all the sanctions and checks, everything bank is required to check.

Mush: That technology has existed for a while now. I mean, we haven't reinvented the wheel here. We've just done a very complicated integration job to facilitate this. But basically what we're doing is allowing anybody in the world to get a US bank account. And by that, in our eyes, we're democratizing access to financial services.

Josh: So, let's just put this in real terms. So how can this help me in this situation? So we have, let's say we have a contractor for example, in the European Union today who has an account in the European Union. And we have a US bank account with a larger US bank. And we need to pay them for work that they do. How would your solution help in that scenario, for either side?

Mush: So in your example, I mean you are a US person, a US company, and you have access to abundant choice of safe, secure, advanced banks, first-world banks. But in order to pay your contractor, if it's in Europe or let's say a third-world country, you're going to have to find a way to send them this money.

Josh: Yeah. Today, we do a wire transfer, which is really cumbersome and costly.

Mush: Because a Venmo, a Zelle or real-time transfer method that exists within the country of the US, does not expand internationally. And your bank will not open an account for this foreign individual either, so you can do a quick peer-to-peer transfer. So it's a wire transfer. There is a fee, it takes time. And depending who the receiving party is, it may get even more difficult for them.

Josh: Yeah. And it's been held up a couple of times, the payment. She's had to go in and prove who she is again to her bank and why she's getting the transfer. And there's been some complications. So you're saying, because in this case, if both of us parties had a Zenus account, that we would, we'd just be able to instantly transfer as if they were a US contractor that we're doing transfers with.

Mush: Peer-to-peer. Real-time, immediately.

Josh: That's amazing. It'd be so much cheaper and less time consuming. So where are you guys in terms of getting this idea out the door?

Mush: So we'd like to consider that we've already tackled the most difficult milestone of our business model. So we have our core team, we have a banking license, we've activated our banking license, which means that the regulators have verified that we can do what we're claiming we can do. And we have the right people and the right capital, and the right infrastructure to support that, from US banking perspective.

Mush: We've just gone into a beta testing and internal testing of our technology. So we're expecting to do that throughout January. And in February, maybe we do a friends and family so we can test our model across various countries. And after that we are planning to go live basically to the public. The first audience that's going to be given a chance to open an account are the leads that we have on our waiting list that we've been accumulating and nurturing using the great technology that KickoffLabs provides.

Josh: So let's talk about that, that waitlist campaign. So you're running a waitlist campaign on our product KickoffLabs. That's obviously how I found out what you guys were doing, and heard about you in the first place. What's been the best part of that for you so far?

Mush: So initially we started, we scratched our head and said how can we tackle this? How can we let the world know that what we're doing is here, right? And we already knew that we're first to the market. And we know that there's going to be a lot of questions about, is this legal? Can we really do it? There's always suspicions when you do, when you're changing paradigms, especially into something so sensitive as banking. You're tasked on safe keeping somebody else's money. It's a fiduciary duty.

We built a nice website and used the waitlist campaign methods that for example, Robinhood had practiced, and the Dollar Shave Club's done. This kind of cool new brands have managed to create FOMO and create, build up this desire.

Mush: So we set out to design, basically we said, let's test the appetite. We think and our research has shown that there's a lot of demand for this in the world. The freelancer market, it's a multibillion dollar opportunity. The cross-border remittance is a multibillion dollar or trillion dollar opportunity. And, in my personal experience, all these broker dealers servicing millions of customers have this same exact problem. How do we facilitate deposits and withdrawals for our clients?

Mush: So we built a nice website and we had seen, and used the waitlist campaign methods that for example, Robinhood had practiced, and the Dollar Shave Club's done. This kind of cool new brands have managed to create FOMO and create, build up this desire. So we said, probably the best way for us to go forward both from cost efficiency perspective, because we're not ready to sell a product, so why spend money on marketing? Let's just put something out there and see what the organic demand is.

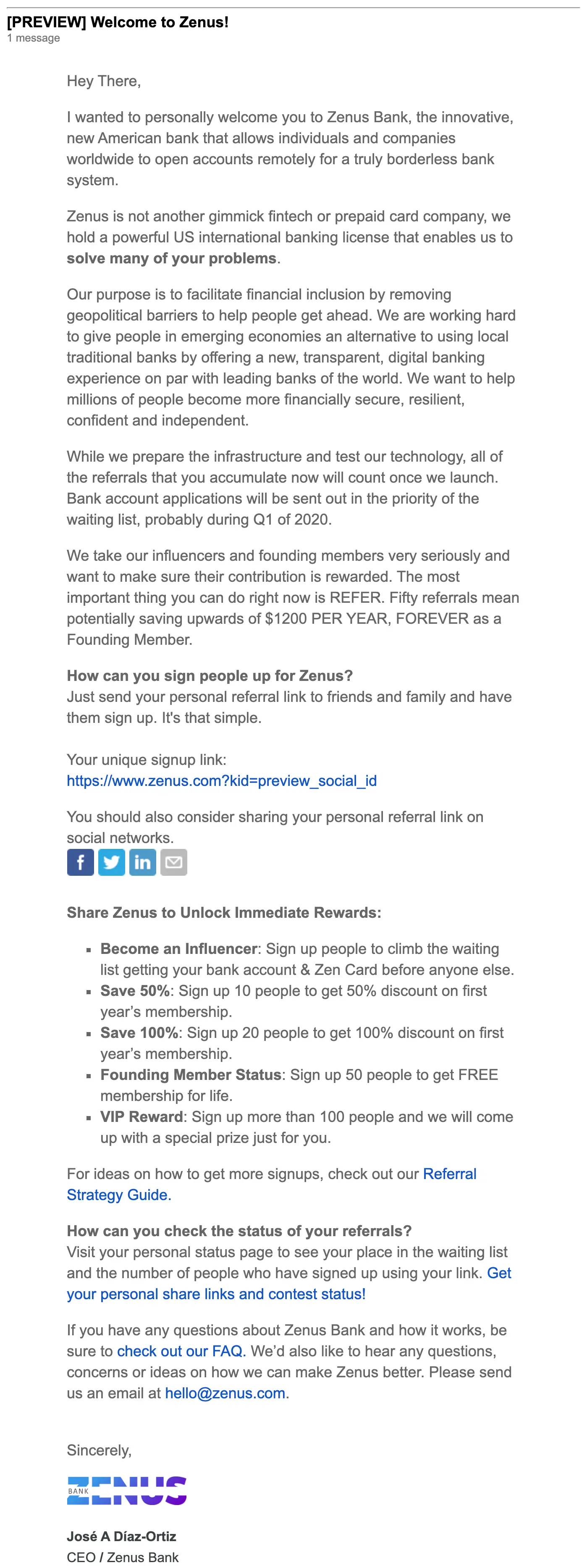

So we picked this waitlist campaign structure that KickoffLabs offers us. Created a one-page website. Very simple and it has a minute-long video. It just says the basic. We're the first US bank that lets anybody in the world open a US bank account. And that's it. We just published it.

Mush: So we picked this waitlist campaign structure that KickoffLabs offers us. Created a one-page website. Very simple. It has a minute-long video, like a commercial of what we do. And I guess it just says the basic. We're a US bank and we're the first US bank, and we let anybody in the world open a US bank account. And that's it. We just published it.

I did I think a LinkedIn post and we did a Facebook post and an Instagram post and a Twitter post, and that's it. And we saw this huge interest from all over the world. I think we have over a hundred countries right now signed up to our waitlist.

Mush: I did I think a LinkedIn post and we did a Facebook post and an Instagram post and a Twitter post, and that's it. And we saw this huge interest from all over the world. I think we have over a hundred countries right now signed up to our waitlist. To date, I think we spent almost no money. We've just done the basics to set up the accounts and to do the SEO work. But we're not buying traffic. And we've let this organic, this message propagate throughout the world organically.

Josh: Yeah. And so I'm not going to share, I won't share some actual numbers, but if you don't mind, I was going to say what's impressive about your campaign from KickoffLabs is the waitlist mechanics seem to be working really well. So you've got about 60% of your leads are coming in as being referred from somebody else. And so that's a great number. And to me that is one of the indicators when people ask, when I'm looking at a product and saying, do you think my product has a market? And I say, well are people telling other people about it, with the sharing links? And in your case they definitely are. You're getting a lot of traffic from those shares. You're getting a high percentage of your leads, I guess that's 60% from the shares. And you have a really good conversion rate.

Josh: And so those are all three strong indicators. One thing I do want to talk about or ask you, and it's a question that comes up a lot from other customers, so this is where you might be able to help some other people listening to this. So your website, your one-page website does a great job explaining the basics. You're basically saying like, here is what the product is. I mean, on your site it literally says "Zenus makes it easy and safe for everyone to access, send and receive, and store money in the United States from anywhere in the world." Which is the perfect elevator pitch to what you just explained. There's a button that says "Join the waitlist." When I do that I get a little pop up, it's asking me to "Secure my spot in the waiting list and participate in exclusive promotions while we approach our go live date."

You don't give a specific date and you don't make any specific promises on this page. You're just saying participate in exclusive promotions on the go live date. And then you are asking for just three relevant things; nationality, name, and email. Simple.

Josh: Something I want to note about this, you don't give a specific date, which is where some people get themselves in trouble. And they don't make any specific promises on this page. They're just saying participate in exclusive promotions where you get on the go live date. And then you are asking for three things on the form and some people go overboard on the form. But I think your three things are relevant. You're asking for nationality, and you have a dropdown, name and email. And presumably what's great about that is the nationality helped you determine the different countries, you just needed to make sure that you're working in or when you sign somebody up for a beta list you might say, well I only want to bring in people from this country first, right? So that information is useful for you guys in terms of planning your product.

Mush: Yeah, yeah, correct. So actually the tools, I'm very happy to talk about some of the tools and how it can help other businesses. The questions, first of all, what we ask is, an email and a name, is for us to be able to contact our customer, obviously. Nationality, it's a custom field we created tromping the visitor to fill in this nationality. Obviously they can lie in here, they can make up something, or this may be where they were born, but they live in a different country. Or it may be that this is the country they live in, but their passport is from somewhere else. Then we rely on the tool that KickoffLabs provides us, which essentially stores the geolocation of the device used to fill this form. And we've seen some interesting statistics in there where there's somebody that's in one country, that fills for example, I don't know, Germany in the field. But the country shows up as United States or Mexico.

We have around 25,000 people on our waiting list. And again, this has been fruits of organic growth. Like you said, 58 almost 60% of leads come from existing waitlist customers sharing their link.

Mush: And what's also interesting is we've had a lot of fan mail from our customers. There's a customer service email that we have and through the various social channels we've been getting feedback from the people that visit our website. And I'm happy to share, we have around 25,000 people on our waiting list. And again, this has been fruits of organic growth. Like you said, 58 almost 60% of leads come from existing waitlist customers sharing their link. So, that's great for us. And, how do you call it? And this has given us a chance to communicate with our clients because we're still building our product. Not every client is going to qualify for a bank account. There are sanctioned countries in the world that us, as a US financial institution, we cannot touch, Iran for example.

Our (waitlisted) clients have given us a lot of new ideas on what we need to focus. Essentially, we're using this tool to figure out what is the low hanging fruit, what is our perfect demographic?

Mush: But at the same time, our clients have given us a lot of new ideas on what we need to focus. Essentially, we're using this tool to figure out what is the low hanging fruit, what is our perfect demographic? Because as a bank, there's, a million types of verticals that we can focus on. And if you're a startup business, you're never going to be good at what you do if you're spread too thin. So, we've basically used this a bit to communicate with our customers and see what they really need. And let me see what was your other question you touched on?

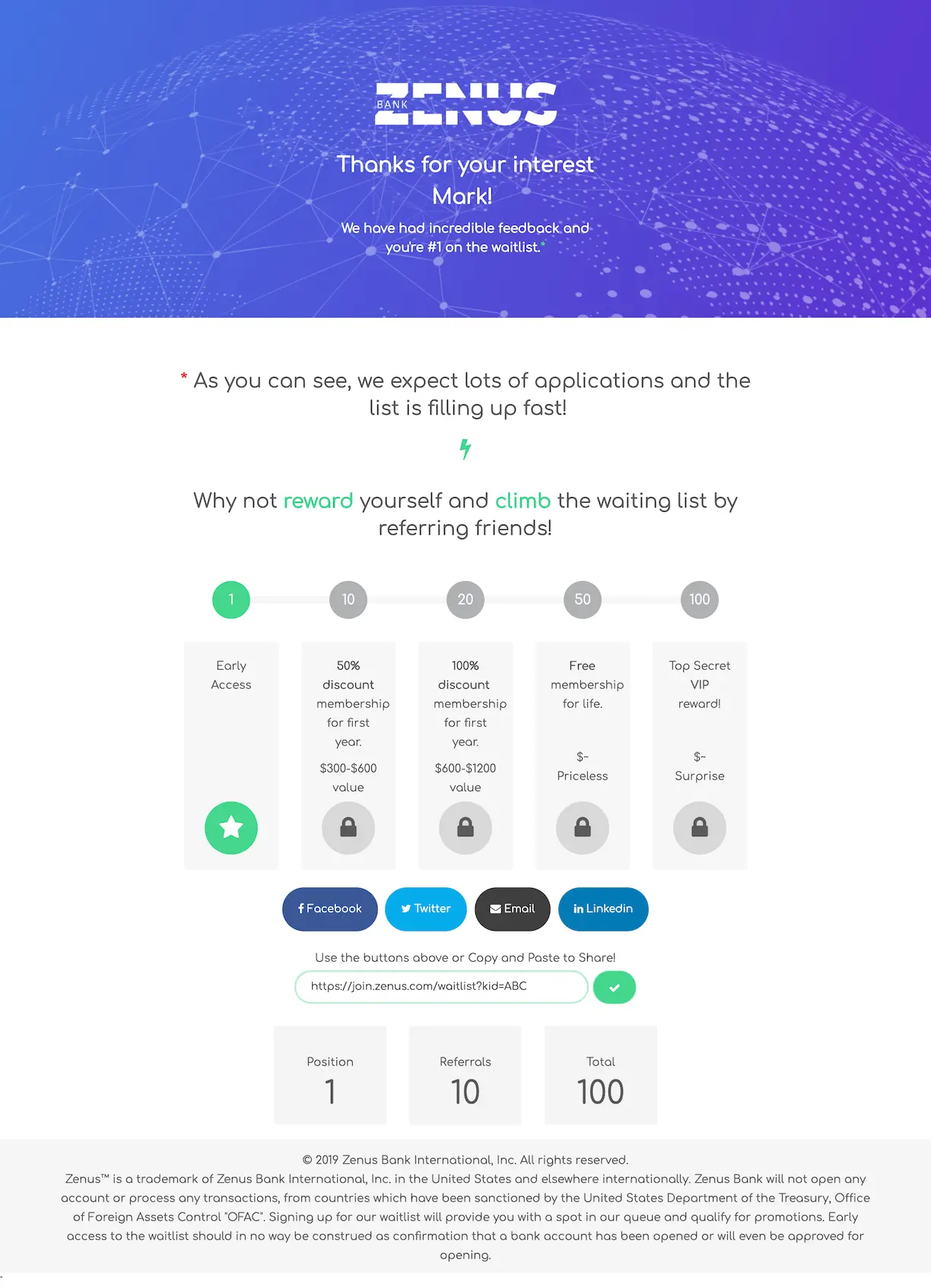

Josh: While you think about that, I want to ask you about the reward page because you're giving people rewards for sharing. And it's a common question, say, how did you come up with the rewards? So I see what you have is, they get one person referred, they get earlier access. Potentially they get 10 points, they'll get a discount membership for the first year, so 50% off. And basically if you have 20 then you give them the whole first year off, it sounds like, their membership. And so how did you come up with the different reward levels there? Because that's a question people ask all the time. Like, what should I set for these things?

Mush: Yeah, yeah, exactly. That's what I was meaning to talk about. So a bank traditionally makes money by lending, right? They take deposits, they collect the deposits and then they lend it out. Lending is not feasible when you're operating cross-border. Right? It's very hard to justify and to follow all the risk matrix. If I take money from Spain and lend it to somebody in China, it's not sustainable. So our business model is to act as a full reserve bank, which means we have zero lending. We're essentially a bank that acts as a wallet to hold customer deposits and allow them to make payments. And by cutting the biggest revenue generator of a bank, we essentially need to substitute that with something. So to be able to survive, to be able to provide this innovative service, we've come up with a membership model.

Mush: So a subscription-based business model. This means that to be able to apply or to have an account, we charge a monthly fee. This fee is not based on how much deposits you do, how much business we do. Because again, we're trying to simplify, standardize and democratize access to financial services. So what we're saying is that an individual customer is going to pay $50 per month. A simple business structure is going to pay $100 a month. So double that.

Mush: If you compare that, if you do a quick comparison, $600 a year for an individual account is quite expensive for you, for example, as an American. But if you are a freelancer working, living in a third-world country, most of your customers are in the US or Europe. Imagine the power of being able to invoice these customers from a US front-end, from a US bank.

Josh: It'd be way more attractive. I'd be more likely to hire that person and keep working with them.

So why not essentially help our initial traffic, help our leads, the first people that discovered us, by rewarding them for doing the marketing for us?

Mush: Exactly. Then it reduces the cost of doing business because a lot of these companies have bills to pay. Now instead of doing international wire transfers, they can do ACH's, they can do free payments using Visa, Visa Direct. They get a US issued Visa card, which is amazing feature. For a value approximately what an American Express Platinum costs, we're giving them access to a US bank account, which they've never been able to have before. But at the same time, we do recognize that it's expensive and eventually we're going to have to spend money to acquire customers.

Mush:So why not essentially help our initial traffic, help our leads, the first people that discovered us, by rewarding them for doing the marketing for us? So we've created a very easy to hit milestones where, first when you sign up you just get for access to this on a waiting list, because we do expect to be somewhat bottlenecked as we go live, because being the new bank, new technology, we're going to try to scale into full growth rather than just opening the flood gates. It's a sensible thing to do.

People that are on our waiting list will get priority. Second of that is the people on our waiting list now are aware that they need to pay $50 every month they want to have this bank account. So what we've done is real simple, refer people and get discounts up to 50 people and then it's free for life.

Mush: Therefore, people that are on our waiting list will get priority. Second of that is the people on our waiting list now are aware that they need to pay $50 to see if they qualify for a bank account and pay $50 every month they want to have this bank account. So what we've done is real simple, refer 50 people and it's free for life. I think the statistics show that an average person has what, 700 friends on social or something like that. I think that's the latest stats. So 50 people, whether it's your actual friends and contacts or clients or business partners or just a random post on social networks, it helps us. It's operational tasks that we don't have to do and a lot of times it's money we don't have to spend, so we're happy to pass on those benefits to the user that act as an affiliate to us.

Josh: Yeah. There's a couple of things you mentioned there that I wanted to highlight that I think work really well across all the different campaigns I see, which is one, you made the rewards easy to understand. So basically, it's one reward, it's how much of a discount are you getting on your membership for this? You scale it up. The second thing I wanted to mention was the levels you pick are fairly achievable, and you're giving a good amount of value for those achievable levels. I think people are scared sometimes to do that, but they don't realize what you said is exactly true. Which is that rather than you having to go and spend a ton of money on Google Ads, they're saving you some of that cost because they're referring you these customers where you might have to spend 100 to $200 to refer to get a customer to sign up ultimately via Google Ads. You're getting this from them potentially at a much cheaper cost, so you're not paying a ton of money for all these additional leads.

Mush: This value in financial services actually goes up to around 1,000 or $1,200, which is the cost to acquire a customer or a lead that converts into a customer. I would say that the rule of thumb in financial services, that's fairly accurate. So for us, waving $50 income per month gets us another 50 customers, potential customers, having to pay that.

Josh: Yep. You've at least made first contact with 50 additional potential customers, which is a huge leg up in terms of being able to market to them and advertise to them and keep them on an email list. So what have you done? Have you done anything? It doesn't sound like you spent a lot of money on advertising the campaign. So have you sent out emails along the way to the people on the list so far?

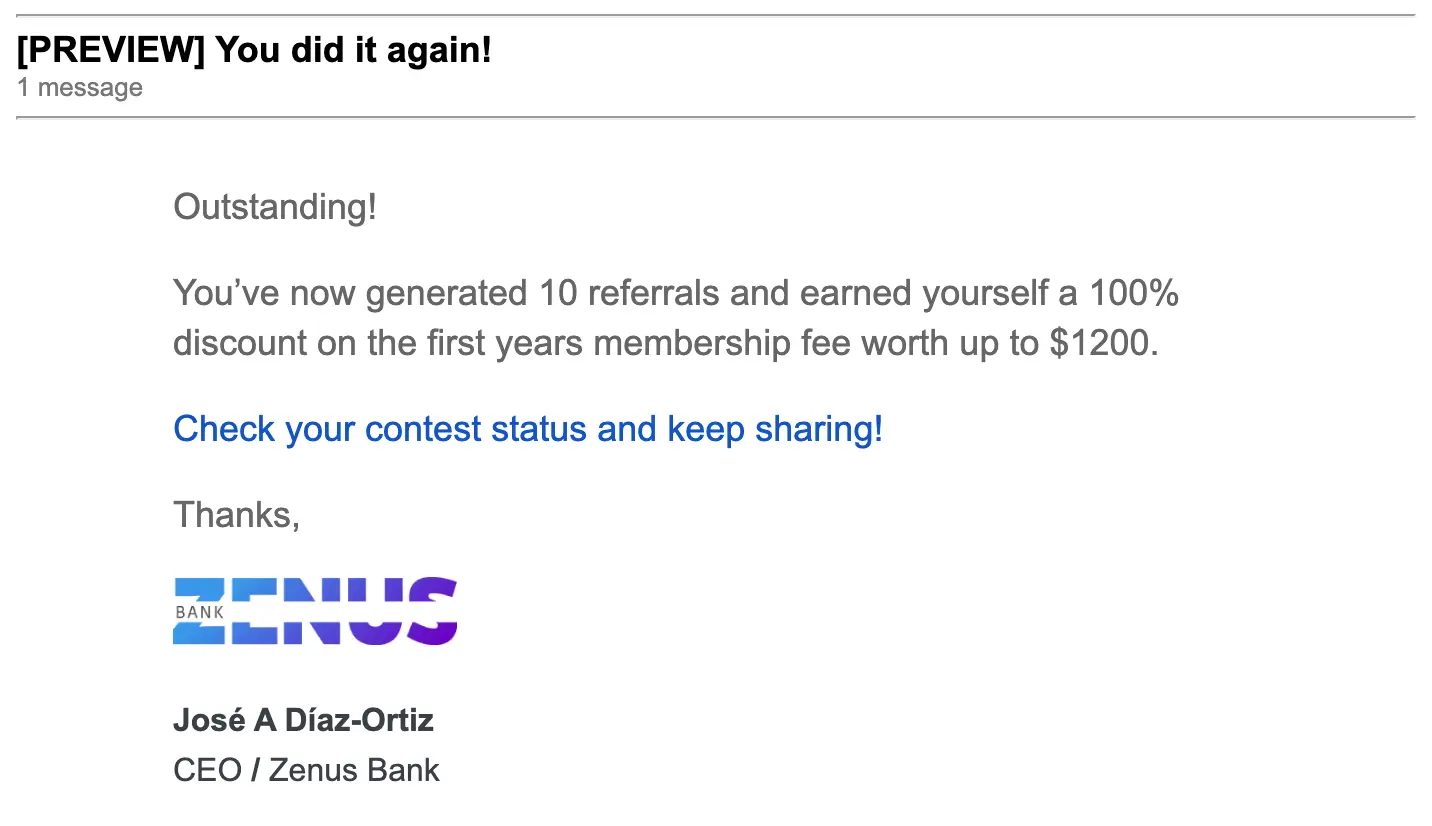

Mush: So we've used one of the good features that you have, which is the automatic congratulate ...

Josh: We call it a reward level email when they get things.

Mush: Exactly, a rewarding level email. So every time you pass a milestone or you save further, we send a thank you email saying congratulations, you've made it, you've saved this much money or up to this much money. Keep trying. You can get more rewards. That's great because I think the system has automatically sent, I don't know, hundreds of thousands of emails and the ... Let me read here. We have 75.9% opening rate of this email.

Josh: Yeah. That's really impressive.

Mush: Amazing.

Josh: Yeah.

Mush: So, we're pretty happy with the way this is going, and like I said, it's not only getting leads but it's gamifying it a bit, creating a reasons for the customer to get in touch with us and learning from whatever they're wanting to get in touch with us for.

Josh: I wanted to call that earlier, because you mentioned it, one of my next questions is what's been the best part of using KickoffLabs for this marketing challenge? It sounds like you've gotten a lot of benefit out of being able to have contact with and back and forth with customers before you've launched your beta's even.

KickoffLabs has saved us a lot of overhead. There's cool tools available and it is very easy for a nontechnical person to configure and use.

Mush: Yeah. I can say that before I used to run almost an internal digital marketing agency in our company that had to do a lot of these tasks manually. Somebody has to code it, somebody has to execute it, somebody has to measure it and KickoffLabs has saved us a lot of overhead. There's cool tools available. Very easy for a nontechnical person to configure and use.

Josh: Thanks. I appreciate that. So now I have five questions I'd like to ask, call them the Fast Five questions. So just first thing that comes to mind, don't need a lot of discussion on each of them, but for you personally, how do you get in the work zone?

Mush: I'm a multitasker. I actually find that I focus more when I'm a bit distracted, slightly distracted. So for me, work is 24 hours. I'm always thinking and brainstorming so I just need to be engaged. My brain needs to be engaged constantly.

Josh: Favorite vacation spot. Where do you go to relax?

Mush: Travel. Any travel to any new place. I love exploring the world.

Josh: That's great answer. Favorite book or podcast?

Mush: Lately it's just been a lot of technical stuff, so I haven't had time to do reading for pleasure. So hard to answer that one.

Josh: You mentioned a lot of technical stuff, things you have to learn. So something you've learned in the last year.

Mush: I've learned that it's a possible to change banking, that you can innovate.

Josh: Another good answer. Finally, someone you look up to, business or otherwise.

Mush: My parents. We were born in Soviet Armenia and they managed to get me all the way to the first world or US and gave me the opportunities to end up here, as a founder and chairman of a bank.

Josh: That's a great answer too. Anything that I should have asked that you feel like we missed out on talking about? Or any advice for anybody else looking to create their own wait list or run a similar campaign that we haven't discussed?

Mush: I think I would go with your first question was, what made me do it? Whether you're doing a job or applying for a job or you're an entrepreneur, the first thing you still have self confidence, to believe in yourself and to believe that you can do it. So it doesn't matter that it's never been done, like what I'm doing, or it doesn't matter that on paper you're not qualified for the job. You need to believe in yourself first before somebody else recognizes that.

Josh: Yeah, I think that's very true. Before we started this business, KickoffLabs, I went to a startup event and there were a lot of people looking to become entrepreneurs there and it was one of the more powerful things. One of the ... Was a guy who's a famous VC and he was there and I was talking to him for 10 minutes and I asked him for his advice after I'd talked to him and pitched to him what I was doing. He just took a piece of paper and he wrote a note on it and he passed it to me and he said, "I'm just going to leave you with this." The note just said, "I give you permission. Do it." It was such a simple thing, but it's true because people don't give themselves enough permission to just say, I'm going to do this or the confidence to do it.

Mush: No, no, definitely. I can respond that by a similar VC thing that I got is that they said, "Look, we cannot invest in this because we're constrained into a box. If you don't fit in this box, we cannot invest. But that doesn't mean that it's not profitable and it's not going to succeed." He said, "Ignore us. Maybe we're the ones who are going to be jealous that we didn't use that opportunity to invest in you." So essentially, don't be afraid to follow the dreams.

Josh: Absolutely. That's a great, great place to leave the interview. I appreciate all of your time today. So anybody listening, if you've got any questions, how can people reach out to you?

Mush: The bank has all the typical social channels. I'm very active. I'm the founder and I'm basically involved in every aspect. I'm not a micromanager, but I need to see how things are developing. So I'm always reachable at this stage and I'm very eager and happy to hear from whether it's startup entrepreneurs to potential clients or business partners of ours.

Josh: Great. So again, thanks for your time today and have a good rest of your week.

Josh: Thanks for listening to today's interview. If you enjoy the On Growth podcast, please write us a review on Apple podcasts and don't forget to hit that subscribe button. If you'd like to run your own viral campaign or set up a wait list for your upcoming business like they did, check out kickofflabs.com. We can provide the landing pages, referral tracking leaderboards and reward level emails required to make your next product launch a complete success.

KickoffLabs Makes Contests Easy

Quickly and easily setup viral giveaways, sweepstakes, and product launches where fans earn points and rewards for referring friends and promoting your brand!

Start For Free Learn more